This page provides a very high level overview of how pensions work. It’s a large topic, so we’ve provided links to further resources throughout. But there are two very important things you must know:

- Never opt-out of a workplace pension. Your employer pays money into your pension – this is part of your salary, which you simply miss out on if you opt out.

- Due to the magic of compound interest, the sooner you start your pension, the less you need to contribute to it yourself.

Contents

Always auto-enrol in your pension ✅

You should make sure you are enrolled in your employer’s pension scheme. This is a minimum of 3% extra pay in exchange for you contributing 5% of your pay, and many companies will offer more.

This money is placed into an investment account for you, which you can access when you retire. Until then, it will grow, both from your and your employer’s contributions and from growth of the investments.

This age access restriction sometimes puts people off joining. However, due to the employer match and tax relief, if you choose to opt out, you don’t simply get the money you would have had in your pension in your pocket now – you’ll get only a fraction of it.

Note: this explanation, and most of the text on this page, describes ‘Defined Contribution’ pensions which are the norm in the private sector. There is another type of pension called ‘Defined Benefit’, which is more common in the public sector (although some do also exist in the private sector too!). If you have a ‘Defined Benefit’ scheme your pension works differently.

Tax relief on pension contributions explained💸

Income tax

You don’t pay income tax on money you put into your pension.

This means that while you would normally pay £20 in income tax for every £100 earned (for money earned within the basic rate tax bracket), and receive £80 in your pay to spend or save, in a pension you can keep the whole £100.

For money earned in the higher rate (40% tax) bracket or higher, the effective tax-relief is at least 40%. In some cases it can be as much as 85% (see our Tax Traps and Tax Efficiency page for more information).

⚠️ In some cases this additional tax relief is not automatic and needs to be claimed.

- Which: Tax relief on pension contributions explained

- Our wiki: Pension, ISA or LISA – which is best?

- Pensions Advisory Service: Tax relief and contributions

National Insurance and Salary Sacrifice

Some employers offer a ‘salary sacrifice’ pension arrangement. This means that instead of you earning £100 and putting it in the pension, they reduce your salary by £100 and increase their contributions to your pension by £100.

This saves you another tax – national insurance, which for most people is charged at 8%. Your employer will also save on their national insurance contributions, and some employers will even pay some or all of that saving into your pension too.

- Salary Sacrifice Calculator

- Salary & Take Home Pay calculator

- Pensions Advisory Service: Salary sacrifice

- MoneyHelper: Workplace pension contribution calculator

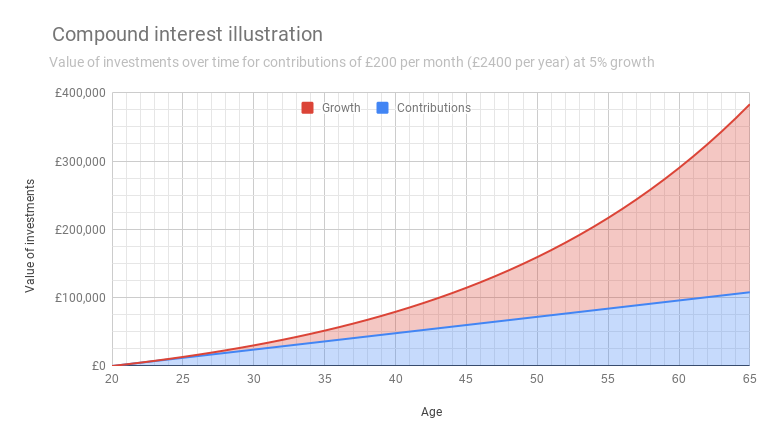

The magic of compound growth 🪄

The earlier you start saving, the more time is on your side. The growth of your savings and investments will compound over time.

When you start investing in your pension, most of the money that is in the account is money you (and your employer) contributed. However with time, growth starts to accumulate, until it becomes the bigger contributor to the total value.

The higher the growth rate % the faster this will happen – we’ve used a reasonably conservative estimate of 5% in this illustration. At 6%, the final value of the portfolio would be £510,584.

Remember that you can only ever start this curve at the beginning. By starting it a year later, the year you will miss out on is the one at the end of the graph. In this scenario, the last five years on the chart provided £127,156 growth!

The longer you wait to start, the more expensive it becomes to catch up. But don’t let regrets about not starting earlier put you off – remember ‘the best time to plant a tree was 20 years ago. The second best time is now’.

Pension growth isn’t the same as savings account interest. Both will compound over time, but there are important differences. Although we talk about growth rates at a certain percentage, this is an oversimplification. In reality the growth will depend on stock markets, interest rates, and all sorts of other factors.

When we talk about average percentages, we’re looking at long-term trends, but 5% average might instead be +10%, -3%, +8% over three years.

For more illustrations of the power of compound interest, see:

- The Calculator Site: Compound interest calculator

- Monevator: Investing for Beginners: Compound interest and its enemies

- Monevator: See compounding in action with this online calculator

- Business Insider: Here’s The Difference Between Someone Who Starts Saving At 25 Vs. Someone Who Starts At 35

Pension calculators 📊

You can use the calculators below to forecast your future pension income at different contribution rates. Your pension doesn’t need to be invested with these companies to use their calculators.

- Pensionbee: https://www.pensionbee.com/uk/pension-calculator

- Vanguard: https://www.vanguardinvestor.co.uk/what-we-offer/personal-pension/pension-calculator

- Aviva: https://www.aviva.co.uk/retirement/tools/my-retirement-planner

- Hargreaves Lansdown: https://www.hl.co.uk/pensions/pension-calculator

Note different calculators will use different assumptions. Take the time to read them to understand how the numbers they provide have been calculated.

The state pension 👴🏽

As of the 2025-26 financial year, the full state pension is £230.25 per week, paid four-weekly, which comes to £11,973 per year. State pension age is about 10 years later than private pension access age.

State pension entitlement is based on your National Insurance contributions. You need a minimum of ten years of contributions (or equivalent credits) to receive any state pension, and the full amount requires 35 years of contributions.

Personal Pensions (SIPPs) 🏛️

A SIPP (Self Invested Personal Pension) is a pension you can open yourself, and manage the investments yourself directly or via a financial adviser. They can often have a wider range of investments available than a typical workplace pension scheme.

If you don’t have a pension scheme through your employer, for example if you’re self employed, it’s important to open a SIPP to save for your retirement.

If you do already have a workplace pension (or pensions) but want to be more hands-on with your investments, you can also open a SIPP for this purpose. You may be able to make partial transfers out of your current workplace pension into your SIPP – check your workplace scheme for details on this and any fees that might be involved. You can also transfer older pensions from previous workplaces to it, and use it for any additional pension savings you want to make above what you normally save in your workplace pension.

- MoneyHelper: Self-invested Personal Pensions

- Legal & General: SIPPs explained

Managing your pensions ⚙️

What happens when I leave my job?

The pension you’ve built up while working at your current job is still yours when you move on. It is normal to build up several pension pots over the years, and you can also combine them if you prefer.

If you’ve received correspondence about your pension to your work email address, make sure to forward it on to somewhere you can still access after you leave.

Should I change what my pension is invested in?

For the most part, the default funds your pension provider selects will work just fine and there’s no need to adjust. However, if you’re interested in optimising it as much as possible, there may be scope to do that, both within your current scheme and by transferring out to another provider if necessary. Take a look at our pages on investing and index funds if you want to get more hands-on.

How do I claim higher-rate tax relief?

This depends on the type of scheme you are enrolled in. If you’re not sure what type you have, ask your payroll or pension provider.

- Salary Sacrifice/Salary Exchange, or Net Pay schemes: you will receive your full tax relief automatically, there is no need to claim additional relief from HMRC. Some workplace schemes will operate on this basis.

- Relief at Source: this means contributions are paid to the pension provider after income tax is paid, and they claim it back from HMRC. They will do so automatically for basic rate tax relief, but higher rate taxpayers will need to claim the additional relief through HMRC’s web service. All SIPPs and personal pensions operate on this basis, and some workplace schemes will also.

If you are a higher-rate taxpayer and reading this is news to you, head to the HMRC guidance page, and come thank us on the Discord for the tax relief cheque you’ll receive once you get in touch with them!

- Hargreaves Lansdown: How to claim higher-rate tax relief

- MoneyHelper: Tax Relief on Pension Contributions

Should I transfer and merge old pensions?

If you have multiple pension pots from different jobs, you may prefer to combine them into one of your existing pensions (or a SIPP) so there are fewer accounts to keep track of.

Your pots will not grow any faster when they are combined. But if your providers have different fund choices and fees, those will have an effect on the outcome. Pay attention to these when working out where to transfer to/from.

In addition, some pension schemes (especially older ones) may offer additional benefits such as an earlier access age, tax-free rights greater than 25%, guaranteed rates or rate bonuses, or benefits for your spouse in the event of your death. Always check if a scheme offers any such benefits before choosing to transfer out of it.

- Which: Should I combine my pensions?

- MoneyHelper: Transferring defined contribution pensions

How do I find old pensions?

If you’ve lost track of pensions you had from previous jobs, don’t fret! They’ll still be there. You just need to find who the scheme was operated by, so you can get in touch to update your contact details with them and find out exactly what you have. To find the name of the provider:

- Check your emails and paperwork for any information

- If your former employer is still operating, contact their HR to ask them

- If you’re in contact with any former colleagues, they might know

- Use the UK government’s Pension Tracing Service

- See MoneyHelper’s page on lost pensions for more organisations and services which can help

- The UK Government is launching a Pensions Dashboard in 2026. Your old pensions should show up there when it’s available.

Frequently Asked Questions ℹ️

‘Half your age’ rule ➗

The most common recommendation for retirement saving is that you should save half your starting age as a percentage of your income – if you start saving for retirement aged 20 you should save 10% of your income for the rest of your working life, if you start age 30 you will need to save 15%. If you leave it until you’re 40 you need to save 20% of your salary.

This includes employer contributions to your pension – so to reach 10%, it could be 6% your contributions and 4% employer contributions.

This ‘rule’ is intended to illustrate the power of compound interest and the value of starting early. It’s a good quick reference point to give you a general idea of how much you might need to contribute if you’re starting from scratch. For a more accurate basis for planning, use the calculators provided above.

When can I access my pension? ⌛

State pension age is currently 66, and increasing to 67 by 2028, anticipated to increase again to 68 by 2039. You cannot start taking a state pension younger than this, but you can delay it to have higher payments in the future.

Currently, most personal and occupational pensions can be accessed at age 55. There are plans to raise this age to 57 in line with the proposed state pension access changes. You will need to check your specific scheme to be sure of what it permits, as they may vary.

If I opt out, how much money will I lose out on? 💰

If you’re considering opting out of a pension, the short answer is ‘don’t’, but the longer answer is ‘calculate how much money you’d be giving up on before you decide’. For example:

If you earn £25,000 per year and you auto-enroll in a pension where you pay 5% with a 3% employer match (the legal minimum), you will pay £78.16 into your pension per month and your employer will pay £46.90. This is calculated using your ‘qualifying earnings‘, which is your gross salary minus £6,240 (this number can change each tax year):

- Your qualifying earnings are: £25,000 – £6,240 = £18,760

- Divided by 12, this is £1563.33 per month

- 5% of this is £78.16 (your contribution)

- 3% is £46.90 (your employer’s contribution)

- Total amount going into your pension each month is: £125.06

If you choose to opt out you will receive £62.57 extra pay per month, compared to £125.06 in your pension.

If you have a higher employer match available, or pay 40% tax, or have salary sacrifice, the numbers for a pension would look even better. Use these calculators to work it out:

And of course because you cannot access the money immediately, there’s time for compound interest to work its magic.

What’s the maximum I can put in my pension? 💪

There is an annual allowance (limit) of £60,000 for gross pension contributions. This includes your contribution, your employer’s, and any tax relief applied. However it is possible to utilise unused annual allowance from the previous 3 tax years.

You can’t contribute more than you earned in a (tax) year.

Very high earners (£200,000+) have a reduced allowance – see our tax traps and tax efficiency page.

If you exceed these allowances, you will be charged tax.

- HMRC : Annual allowance

Carry forward

You can carry forward unused annual allowances from the last three tax years for use in the current tax year, allowing you to contribute more than your annual allowance if the following are true:

- You earn at least the amount you wish to personally contribute (including any regular employee or personal contributions in the tax year).

- You have been a registered member of a UK registered pension scheme in each of the tax years you wish to carry forward.

Any used carry over is allocated to the earliest tax year possible.

You can find a detailed explanation of carry-forward, along with examples, at the MoneyHelper page.

I want to retire early. Do I still need a pension if I’ll retire before I can access it? 🔥

Absolutely!

If you intend to stop working at e.g. age 45, that means you’ll have approximately 10 years of expenses to fund before pension access age (ages 45-55), and approximately 40 years after it (ages 55-95). Given the employer match and tax advantages of pensions, you will reach your total savings required much faster if you use them efficiently.

- Monevator: How pensions will help you reach financial independence quicker than ISAs alone

- Monevator: SIPPs vs ISAs – Pensions win if you’re saving for retirement

I’m on track to hit the Lifetime Allowance (LTA), should I stop contributing to my pension? ⏳

The lifetime allowance is in the process of being removed as of 2024, with full removal planned from April 2024. This section has been left here for information.

The LTA is currently £1.073 million and is intended to rise with inflation, although it has been frozen until 2026. If your pension value is higher than the LTA you will pay tax for breaching the allowance. Working out the amount of additional tax you will need to pay can become very complicated due to the way pension funds are ‘crystallised’, but you will never end up ‘worse off’ as your pension value grows.

If you are close to retirement and the LTA is a concern you may (read: will) want to get professional advice on how to organise your pension drawdown to minimise your tax burden. A fixed fee advisor is well worth paying for here to ensure things are in order.

If you are still some way from pension access age but have calculated that you may hit the LTA by the time you get there, don’t panic! Most importantly, don’t opt out of a pension scheme that includes employer contributions – this ‘free money’ is always worth more than the tax penalty for breaching the LTA. If you are currently contributing above what is required to receive your employer’s contributions, you may wish to redirect some of your savings into your ISA, or potentially a General (taxable) Investment Account if you are already using all your ISA allowance.

Meaningful Money have a very thorough video about the LTA: https://www.youtube.com/watch?v=7kErytIUmeo

Why am I not automatically enrolled? 🤷

If you’re employed but haven’t been automatically enrolled, it means you’re either too young or don’t earn enough. You’re almost certainly still eligible to join, but will have to opt-in. Speak to your employer.

What if I’m self-employed? 🖥️

If you’re self-employed you will need to arrange your own pension scheme. This is a higher priority than it would be otherwise.

I’m in a Defined Benefit pension scheme 🦄

Lucky you! Just don’t opt out and you’re good to go 🙂

Note that a lot of the explanations and advice on this page don’t apply to you. Take the time to read and understand the details of your specific scheme, whether it’s NHS, LGPS, USS, alpha, Teacher’s Pension Scheme, etc. There will be guidance available from the scheme, and you can also speak to your union if applicable.

…Seriously though, don’t opt out. Sometimes people do some back-of-the-envelope calculations and think they can beat their DB pension with personal investments. This always relies on an underestimation of the value (and price) of a guaranteed income that a DB pension provides.

- MoneyHelper: Defined Benefit pension schemes explained

Helpful resources 📚

- MoneyHelper: Pensions and Retirement includes explanations of different pension types, saving for retirement, how to take your pensions, getting financial advice and more – recommended!

- Gov UK: Plan your retirement income: step by step

- Gov UK: PensionWise site, for those close to or at pension access age