If you have savings available, is it better to overpay your mortgage, or use the money to save or invest?

There isn’t one right answer to this question. As always with personal finance it depends on your individual circumstances and future goals.

Before considering either option, make sure you’ve checked the flowchart and:

✅ you have a full emergency fund

✅ your short term goals are funded

✅ your pension is on track for a comfortable retirement

If any of these are not yet in place, it’s not even a contest!

Contents

How do mortgage overpayments compare to savings or investments? ⚖️

Mortgage overpayments vs cash savings 🏦

Mortgage overpayments provide a guaranteed, risk-free return of the interest rate on your loan.

Cash savings (in a bank savings account or cash ISA) also provide a risk-free, guaranteed return.

This makes them directly comparable to each other. In fact, if you had a savings account with the exact same interest rate as your mortgage, putting your monthly savings into one or the other would give identical results. So this dilemma is very simple – the highest interest rate wins.

If you can find a savings account with a higher interest rate than your mortgage, you will be financially better off saving there than overpaying your mortgage. If your mortgage interest rate is higher than available savings accounts, you are better off overpaying your mortgage than holding savings.

The bigger the difference between the two rates, the bigger the difference in your return.

When you’re comparing the rates, bear in mind that you may need to pay tax on interest earned from savings. If so, you’ll want to compare the rates after tax.

Mortgage overpayments vs investments 📈

In practice, to substantially beat your mortgage’s rate, you would usually have to invest in assets which carry some risk.

This ‘risk’ applies to both short term fluctuations in value, and the fact that investment returns are not guaranteed the way a bank account interest rate is. Historically, long term investments have provided an after-inflation return of 1.6%-5.1% per year (that’s 1.6% for bonds and 5.1% for equities. Most portfolios will have a blend, to balance investors’ requirements for stability vs growth). So as an approximation, assuming 2% inflation, we can say the average nominal returns are in the range of 4-7%.

Since mortgage borrowing also tends to be long term, it’s not unreasonable to compare mortgage interest rates to long term investment returns. But it’s still apples and oranges – a certainty vs a probability. Many people would value an investment which was guaranteed to return 4% each year over one which has a solid track record of returning an average of 4%, or even 7%.

This is why it is generally only when your debt is at low interest rates that investing starts to become more attractive than debt repayment.

What other factors should you consider?

Mortgage overpayments are illiquid 🧱

When you make a mortgage overpayment, you lose access to the money. To get it back into your bank account and spend or invest it you have to re-mortgage your property, which costs money and takes a minimum of a few weeks to arrange. You can’t sell a brick or two of your property to make ends meet!

In contrast, cash savings and investments are very liquid. Having your money more readily available could be an important benefit of choosing to save outside your mortgage. You can also easily change course and use your savings for mortgage overpayments, for example if facing an interest rate increase.

On the other hand, having your savings accessible could be a disadvantage, if you end up reaching into your savings frequently or for unimportant things. That temptation isn’t an issue if you have overpaid your mortgage.

Mortgage overpayments are tax-free 💰

Interest you receive from a savings or investment account may be subject to tax. But there’s no tax on the ‘savings’ you make by overpaying a loan.

In practice, between the ISA allowance, Personal Savings Allowance and Capital Gains Tax allowance, most people in the UK won’t pay tax on savings interest or investment growth. However if you do, you should factor this in to your calculations, and compare your mortgage interest to your post-tax returns from savings or investments.

ISA allowances are use-it-or-lose-it ⌛

Your ISA allowance resets every year. This means it’s valuable to use as you go along, especially if you are close to maxing it out, or could be in the future.

Mortgage overpayments carry a psychological benefit 🧠

Many people who have fully paid off their mortgage say it’s one of the most exciting and satisfying financial milestones they have achieved. Removing your largest monthly bill can feel liberating, freeing you up for other goals.

This needs to be given proper consideration against a potentially more financially “optimal” solution.

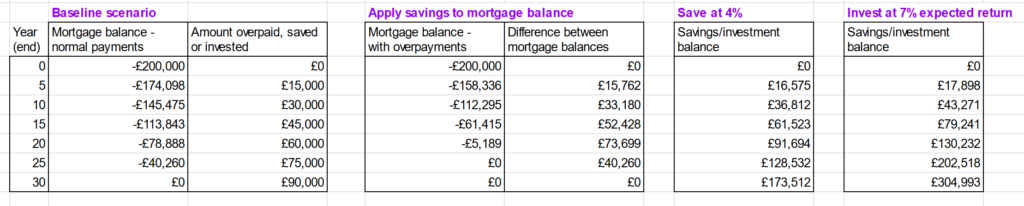

Example illustrations 🧮

The table below illustrates a 30 year, £200,000 mortgage with a 2% interest rate, resulting in payments of £744 per month. This person has an additional £250 per month available for long term savings. They are considering using it to:

- Scenario 1: Overpay the mortgage by £250 per month

- Scenario 2: Save £250 per month in a bank savings account, which we’re assuming provides 4% interest.

- Scenario 3: Invest £250 per month. We’re assuming an equities based portfolio with an expected return of 7%.

As you can see:

- Overpaying the mortgage saves tens of thousands of pounds and ends the mortgage 9 years earlier than originally scheduled.

- With savings beating the mortgage rate by 2%, the savings interest accumulates faster than the savings from overpaying the mortgage. The mortgage could be paid off with the savings balance 11 years earlier than originally scheduled.

- With investments returning higher growth than the savings account, the balance builds even faster than the savings account and overtakes the mortgage 13 years earlier than scheduled.

- The bigger the gap between the rates, the more dramatic the difference between the results. Every 0.5% makes a huge difference.

- The longer the time period, the more those differences build up. They are not nearly as significant over 10 years as they are over 30.

If you’d like to edit the table displayed above you can copy it from here.

There are also online calculators available to make similar calculations:

- https://www.hl.co.uk/tools/calculators/regular-investing-calculator

- https://www.moneysavingexpert.com/mortgages/mortgage-overpayment-calculator/ (enter your expected investment return as savings interest)

Remember, you don’t necessarily have to pick one or the other. You may decide that going all-in on finishing the mortgage early or building an investment portfolio is right for you, but you could also do a bit of both if you prefer. You can also adjust your allocation as interest rates change over the years.

Should I overpay to improve my Loan to Value (LTV) and interest rate? 💸

The simplified table above assumed a consistent interest rate of 2% throughout the life of the loan. However in reality lenders offer better rates the smaller your loan is in comparison to the value of the property. The LTV thresholds for better deals can vary, but tend to be 95%/90%/80%/75%/60% (with no further change past 60%).

If by overpaying £10,000 your interest rate drops from 2% to 1.5% on a £200k loan, that’s an interest saving of £1,000 per year, which is roughly equivalent to a 10% PA return, in addition to the interest saved on the repayment amount itself!

If your mortgage is close to renewal, and your LTV is close to a threshold that will give you a better rate, you should consider the benefits of this course of action.

Should I overpay now in case of higher interest rates in the future? 🔮

In general it doesn’t make good financial sense to make decisions today based on possible future changes. Fear of future interest-rate increases is not a great reason to overpay a mortgage. If an interest-rate rise were to happen, you could change your strategy then.

What if I have received a lump sum? 🧧

If you have received a lump-sum, the decision-making process is the same as with regular overpayments.

You may also be interested in reading our page on lump sums and windfalls.

Never pay fees to overpay ❌

Many mortgage deals charge an ‘Early Repayment Charge’ if you overpay more than a certain permitted amount.

This charge only applies during your fixed rate period. If you’re overpaying high enough amounts that you will incur an ERC, it is almost always worth holding off until you can overpay for free, such as during the process of remortgaging. (Simply remortgage for a lower amount, and pay the difference using your savings).