Whether you’re thinking about what to do with your savings or your time, it’s often taken as a given that ‘passive income’ is the best goal to pursue. For many people the term has become synonymous with success, wealth, or any type of investing.

In reality, this is not the case, and searching for free income can actually be counter productive.

Contents

Why do so many influencers talk about passive income?

The short answer is: because it’s a really attractive idea. Who wouldn’t want to receive income without needing to work for it?

Because it has such a widespread appeal, low-effort personal finance books, videos and podcasts will often focus on this topic. Selling the passive income dream is a very profitable line for influencers, so it is in their interests to promote it as the best route to success – or even the only one, with working for money dismissed as a mug’s game.

At this point the phrase has basically become a meme, and a red flag that someone is trying to sell you something.

Looking for ‘passive income’? Look out for scams

If you are looking for opportunities to make passive income you will quickly find that there’s a whole universe of content on this topic, with many niches for different audiences. Whether they emphasise that it’s easy and anyone can do it or that it’s difficult and requires grit and determination, whether they promise riches or just a small stream of income, whether they suggest the best money is in affiliate links or crypto trading, it is all different marketing for the same basic idea.

Influencers promising passive income will try to sell their audience on bogus training courses, access to ‘exclusive’ communities, personal coaching, trading tips, or any number of other products they think you might be willing to pay for in the hopes you can replicate their apparent success.

The truth is that you will never be able to, because these influencers are actually making their money from their audience, not from whatever activity they claim made them wealthy (and that they will kindly teach you for a fee).

They are also often lying about their wealth and income to appear more successful, and thus more aspirational and credible.

I feel like I don’t earn enough – how can I increase my income?

If you would like to increase your income, the most efficient way to do this is generally through your main job. It is almost always better to look for career progression opportunities than ‘passive income’ or ‘side hustle’ opportunities. Finding a role that pays £5,000 more will likely be easier to achieve, more reliable, and take up less of your free time than trying to make £5,000 elsewhere, and investing in your long-term employability will compound over time.

If you need more income in the immediate term to keep up with costs or goals, the simplest solutions are things like overtime at your workplace, or getting an evening or weekend job.

If you are currently at school or university, make your studies your priority, alongside researching career opportunities. To learn more about personal finances, our flowchart is a great place to start.

I have savings – shouldn’t they generate an income?

If you’ve recently started building savings, or perhaps received a lump sum, your first thought may be: can this provide some income?

It makes sense to want to see some tangible benefit from your savings. But the issue with focusing on receiving ‘passive income’ from your savings is that by taking income out of your investments rather than re-investing it, you lose some of the magic of compound growth. See the “dividend portfolios” section below for an example of the impact of this.

Taking money out to spend now means having less money available in future. The more you take, the bigger the impact. It sounds obvious when stated that way but it’s easy to miss.

Gains from interest, dividends or growth are not ‘free money’ – they are ultimately no different to any other money you have or earn. Spending £500 of savings interest has exactly the same effect on your finances as spending £500 of your savings, or £500 of your employment income. (For those interested in digging deeper into this topic, it is called the fungibility of money).

Take the time to work through our flowchart and lump sum guide and make a financial plan that takes into account your income, savings, and goals. This will help you work out how much of your savings you may wish to spend when, and at what age you might have enough saved to live off (i.e., retire).

Common passive income suggestions

Making money online

The appeal of this is obvious – make money from your own home and in your own time.

‘Online’ is obviously a broad description that could cover all sorts of activities such as:

- Freelance professional work (disclaimer: that’s just plain work!)

- Affiliate marketing commissions (disclaimer: difficult to make sales unless you already have a relevant audience)

- Selling creative works such as ebooks, apps, printables, sewing patterns, etc (disclaimer: also difficult to make sales in a crowded marketplace)

- Drop-shipping – setting up a storefront that automatically ships from cheaper retailers overseas (disclaimer: trading standards rules make this hard to do legitimately, you are in competition with huge businesses like aliexpress and temu)

- Trading crypto or FX (disclaimer: basically gambling and a great way to lose all your money)

It’s important to remember that even online, truly ‘passive’ income is rare. Most opportunities involve being paid for your work (time, effort, and skills), and will require active effort and maintenance.

This area is particularly rife with scams. If something sounds too good to be true, it probably is. Legitimate niches will likely already be saturated with other people hopeful of making money in them.

Buy to let

Our Buy to Let page compares BTL to investing in stocks and shares. For many people, BTL is not very tax efficient, or particularly “passive”. It tends to take more time and effort than people guess, and may not provide the best post tax returns, so if you are considering this make sure to consider the issues carefully.

Living off investments

Living off savings and investments is very much possible – it’s called retirement! The difficulty is that it takes far more in savings than you might expect. This is why it takes most people several decades to save enough to retire safely.

Exactly how much income you can take from your investments to avoid running out within your lifetime is not a simple question, and depends on many factors. However for very quick (napkin level) calculations, a reasonable number to use is 4%. That means an investment of £100,000 could return an income of £4,000 per year, or £333 per month. Replacing a full income therefore requires a very hefty sum.

If you are still earning and saving, you are better off letting your savings grow than taking income from them to spend. The longer you can leave them alone (and the more you can add to them) the sooner you will build enough savings to make the switch to living off them.

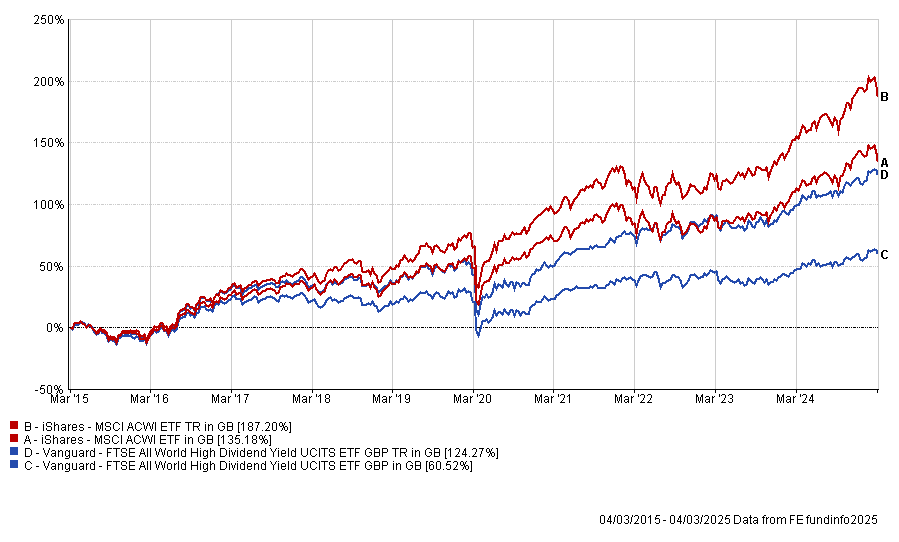

Dividend portfolios

Dividends often appeal to income-focused investors. Spending dividends can feel less painful than selling some of your stock.

But dividends are not ‘free’ – by taking them out to spend rather than re-investing them, you will slow your growth.

The other challenge is that you significantly limit your investment universe by prioritising high dividends investments. For example, an investment that returned 6% growth would be better value than one that returned 2% growth and 2% dividends. Prioritising dividends is a form of active investing, and the research on its drawbacks is conclusive.

The example chart below shows the results of investing £100,000 10 years ago in a global index fund (in red), and in a high dividend yield fund (in blue), with dividends reinvested or taken as income:

| Investment | Results of investing £100,000 from March 2015-March 2025 |

|---|---|

| MSCI All-World index – dividends reinvested | £289,549 |

| MSCI All-World index – dividends taken as income | £237,103 final value £40,109 dividends taken Total £277,212 |

| FTSE All-World High Dividend Yield index – dividends reinvested | £227,839 |

| FTSE All-World High Dividend Yield index – dividends taken as income | £163,070 final value £41,533 dividends taken Total £207,570 |

Starting a business

Owning a profitable business certainly has a higher possible income ceiling than working as an employee. However it comes at a high risk – most startup businesses fail.

There is also no one business that anyone can reliably succeed at, even if you have start up capital to spend. Someone who can run a restaurant can’t necessarily run a marketing agency or a construction business.

If you have an idea that you think you could develop into a successful, scalable business, we’re not here to tell you otherwise! But do plan carefully and realistically, and consider whether the time and effort spent on a project like this will be worth the returns. Start-up costs, running costs, time costs, and opportunity costs (what else could you be doing with this time, effort and money?), all need to be weighed up.

If your starting point is not that you have a potentially viable business idea, but rather that you have money and are looking to get the best returns from it, searching for business ideas is unlikely to be the way to go.